About 10 years ago, when she was 44, Eve Madalengoitia had a hunch that something was wrong. She was experiencing concerning symptoms of the lady sort, and her doctor said it's probably nothing, but let's get you an MRI to be sure. At the time, she was working as a consultant from her home base in Poughkeepsie, writing grants and fundraising for nonprofits; her husband was a self-employed artist. They didn't have health insurance. The expense of an MRI (ballpark $2,600) was so daunting that Madalengoitia convinced herself that her symptoms were nothing to worry about. She was young and healthy, wasn't she?

A few months later she got insurance through a new job, so she went ahead and scheduled the exploratory test. Soon after, she received some news that no one expected. "I had aggressive, high-grade uterine cancer, which was not common in women my age," she says. "I needed immediate surgery, chemo, and radiation." Thankfully, her insurance paid for it, and now she is NED (no evidence of disease). But she is keenly aware of the what-ifs. "Without health insurance, I probably wouldn't have gotten the test and the cancer would have spread," Madalengoitia says. "I wouldn't be here to tell my story."

Madalengoitia's experience is pre-Obamacare, but even people who have health insurance often forgo medical tests and treatment because of high deductibles, coinsurance, copays, or all of the above. Even for those with employee-provided insurance, out-of-pocket healthcare spending has increased by more than 50 percent since 2010, according to human resources consultant Aon Hewitt. Medical debt is the number one reason why Americans file for bankruptcy, according to financial services company The Motley Fool.

We may pride ourselves on our high-quality medical care, but Americans spend almost twice as much money on it, as a percentage of our economy, than other advanced industrialized nations ($3.3 trillion, or 17.9 percent of our GDP in 2016). And we're no better for it: Our health outcomes are poorer and we die younger than citizens of other wealthy countries. It's not the amount of healthcare we consume that is the problem: It's the cost of healthcare. As long as big pharma, big insurance, and big hospital networks are calling the shots, we're unlikely to see these costs go down. And as long as we skimp on social services for our underserved populations, many experts say, we're unlikely to see our life expectancy go up.

A Little-Known Bill Is Gaining Momentum

When it comes to troubling scenarios like these, our lack of universal healthcare is the elephant in the room: It's a huge marker for our poor health outcomes and financial dire straits. We're the only major industrialized nation in the world that does not have universal healthcare. After Hillarycare was famously shot down during Bill Clinton's presidency, the idea receded from the public discussion. It didn't get major play again until Bernie Sanders made his Medicare for All proposal a cornerstone of his rousing campaign in the 2016 Democratic presidential primaries. President Trump's potshots to the Affordable Care Act are not helping to keep Americans insured—but they may be pushing states to devise their own solutions. Several states, including Sanders' home state of Vermont, have made or continue to make efforts to design single-payer programs. What many New Yorkers don't realize is that the Empire State, too, has a single-payer bill floating around in Albany.

It's called the New York Health Act, and it is not new: First proposed in 1991, it's been through many incarnations. In its current form, the bill has p-assed in the State Assembly by a wide margin for the past three consecutive years. Yet a Republican majority in the State Senate means the bill has not made it out of the health committee and onto the agenda for a vote. That could change quickly, as the bill has 31 co-sponsors in the 63-seat State Senate, and only one more co-sponsor is needed to tip the balance.

"The healthcare system is rigged against working people, and the Trumpadministration is working to make healthcare access even worse," says Assembly Health Committee Chair and bill sponsor Richard N. Gottfried, who originally authored the 1991 bill. "New York can do better with an 'improved Medicare for all' single-payer system that covers all of us and is funded fairly. Support is growing with the public and in the State Senate. I expect the Assembly will pass the bill again this session, an important step as we continue to build support for universal healthcare in the face of the Trump agenda."

Meanwhile, State Senator Gustavo Rivera says he and his colleagues are working to get the bill's 32nd co-sponsor. If the Democrats can reach a majority, Rivera will be the ranking member of the Senate Health Committee, and his next step will be to get the bill on the agenda and eventually onto the governor's desk. The bill would cover all New Yorkers regardless of income, preexisting conditions, or immigration status. "We don't believe that your wealth should determine your health," says Rivera.

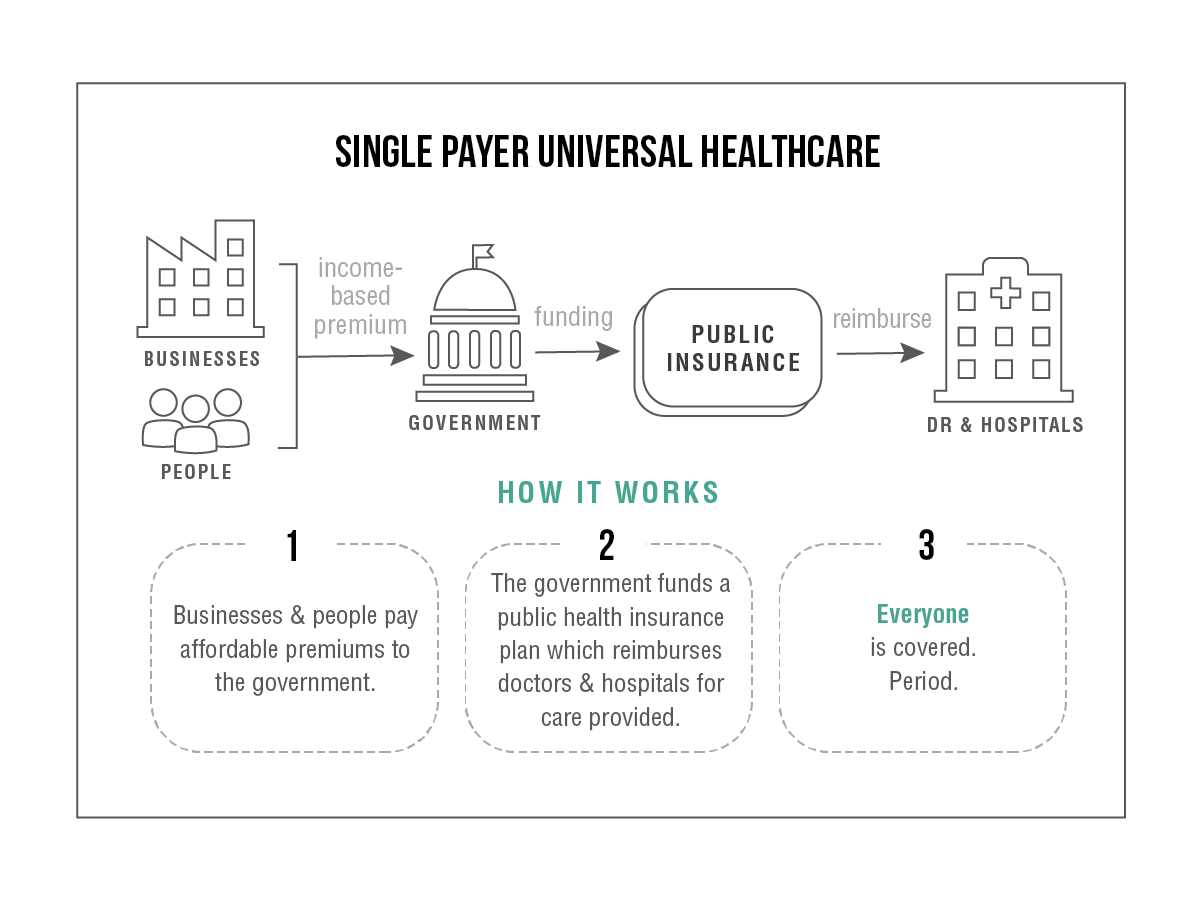

Individual costs for New York's proposed single-payer plan would come from a progressive taxation scheme: The amount that you pay is based on your income and tax bracket. A 2014 study of the New York Health Act by the University of Massachusetts at Amherst estimated that people making under $25,000 a year would pay nothing; those making $50,000 would pay $2,250 a year; and those making $75,000 would pay $5,000 a year. Of those amounts, the employer would pay 80 percent and the individual would pay 20 percent. For wealthier individuals, the estimated amount increases incrementally according to tax bracket, but doesn't rise to infinity. Over 98 percent of households would spend less on healthcare than they do now. Because the funding mechanism is through taxes, there is no "opting out" of the single-payer plan. Additionally, funding from the federal government, which the states already receive for Medicaid and Medicare, would be essential to keeping the program affordable. "You pool everyone's risk together, and therefore you lower the cost for everybody," says Rivera.

Private Insurance–Induced Stress Disorder, a Modern Malady

A single-payer plan would do away with the private insurance companies—removing the middlemen along with their CEO salaries and bonuses, as well as the enormous associated administrative costs. But these behemoths are not likely to go down easy. The most formidable hurdles to making single-payer a reality are moneyed interests like big insurance and big pharma, which sets our country's sky-high drug prices. If the New York Health Act does pass in the state legislature, we can expect these big guns to fight back with a disinformation campaign that plays into people's fears.

That's why educating people is essential. "There's a century of propaganda and a history of making people afraid of universal healthcare," says Katie Robbins, director of the Campaign for New York Health, a grassroots coalition with the goal of winning single-payer healthcare for New York State. "The public is wising up to this, and most people across party lines now believe that healthcare is a right. Premium costs are rising faster than inflation, yet we're getting skimpier plans every year. People are so frustrated."

While Americans no longer seem to fear "socialized medicine" (a misnomer), many do fear big tax bills. While it's true that tax bills would go up under a single-payer plan, the cost of private health insurance would be eliminated, resulting in a net savings for most people. A single-payer plan would also do away with copays, deductibles, and other cost-sharing, because the revenue from taxes and federal support would entirely replace the payments charged by today's health plans. To some extent, New York would have to set up a bureaucracy to handle a single-payer system, but it has one already for Medicaid and Medicare, and we'd see an administrative savings due to the reduced billing complexity of having fewer plans.

"A person who is uninsured can't afford primary care, so when they have a problem they go to the emergency room, which is the most expensive kind of care," says Rivera. "And guess who pays for that? Taxpayers do. So we're paying for it already." A single-payer plan would open the door to primary care for all, and from a cost perspective, it's leaner. "Research studies have calculated the cost to be about $45 billion less than we now spend," says Rivera.

A View from Inside the Healthcare Mess

Support is growing for single-payer healthcare among doctors and other providers, who get to see the dysfunction of our current system on a daily basis. "When you have a heart attack or stroke, your whole life falls apart," says Jess Robie, a registered nurse who works at HealthAlliance Hospital Broadway Campus in Kingston. "This is not the time to argue with your insurance company about what is and is not covered. Why does someone who is not a doctor and has never seen or talked to you get to make that choice? It's insane to me. Families fall apart over this stuff."

On a single-payer plan, the insurance companies don't decide what's covered, and neither does the government. "You and your doctor decide on the treatment you need to have," says Rivera. "Your doctor doesn't need to check and see what's covered. If you're in the system, it's covered." The proposed plan would also cover dental, vision, mental health, and long-term care. This is a game-changer for the average working person. "We're not talking about people who are living off subsidies," says Robie. "We're talking about people who are employed, people who are busting their butts and not making enough money for health insurance. When you have to choose between putting food on your table and paying medical bills, that's not a choice you should have to make."

While the fight for single-payer healthcare is gaining momentum, Rivera says it could take a long time to jump through every hoop required to set a plan in motion. "It could be years away, but the battle is worth waging." Before Canada implemented single-payer healthcare nationwide in 1968, it started in one province, Saskatchewan, and spread to the rest of the country over a 10-year period. In the US, the path is likely to begin in one state. New York could lead the way.

It's going to take a concerted effort to stand up to big insurance and big pharma. Madalengoitia and Robie both volunteer for the Campaign for New York Health to help spread awareness about the New York Health Act. Madalengoitia wants to make sure that others don't put off going to the doctor because of cost and play roulette with their health the way she did. "I wouldn't have thought that would happen to me," she says of her cancer ordeal. "People think, 'Why should I pay for somebody else's insurance when that's not going to happen to me?' The reality is that we all pay for it anyway."

Robbins encourages supporters to get involved: Call your state senator and assembly member, and go to Lobby Day in Albany on June 5 to rally for the New York Health Act. (The Campaign for New York Health has buses available.) Tell your story, have conversations with neighbors, and speak up for universal healthcare as a human right—and the right course of action for a first-world country.

RESOURCE Campaign for New York Health

Support The River! We are a brand new ad-free community newsroom: Help us get the word out by sharing. And consider becoming a paid reader-supporter. Pledge any amount that works for you—it's the best way to show us you like what we're doing!